If you’re thinking about offering your customers financing, this article covers the three approaches to offering customer financing – a buy now pay later (BNPL) company, a traditional consumer financing company, or do it yourself (with easy to use software like Paythen). We discuss the pros and cons of each approach below.

Outsource customer financing to a buy now pay later company (more $$$ and higher fees, if you’re eligible)

A popular way to offer customer financing for businesses that are eligible is outsourcing it to a buy now pay later company like Klarna, Affirm, or AfterPay. With this approach, while it’s easy to get started, you do pay a much higher fee, and give away your customer relationships to these companies – your customers essentially become their customers over time. You also have no flexibility in how you structure your customer financing – you can’t decide billing intervals, amounts, or anything else. You take what they give you. You can’t even cover their fees by adding a surcharge.

In exchange though, you take on zero risk since you get paid upfront and can get additional sales driven by these platforms. Over time, it is common to lose your customers to these very platforms though as they become shopping super-apps and encourage shoppers to begin their shop on their sites (instead of yours).

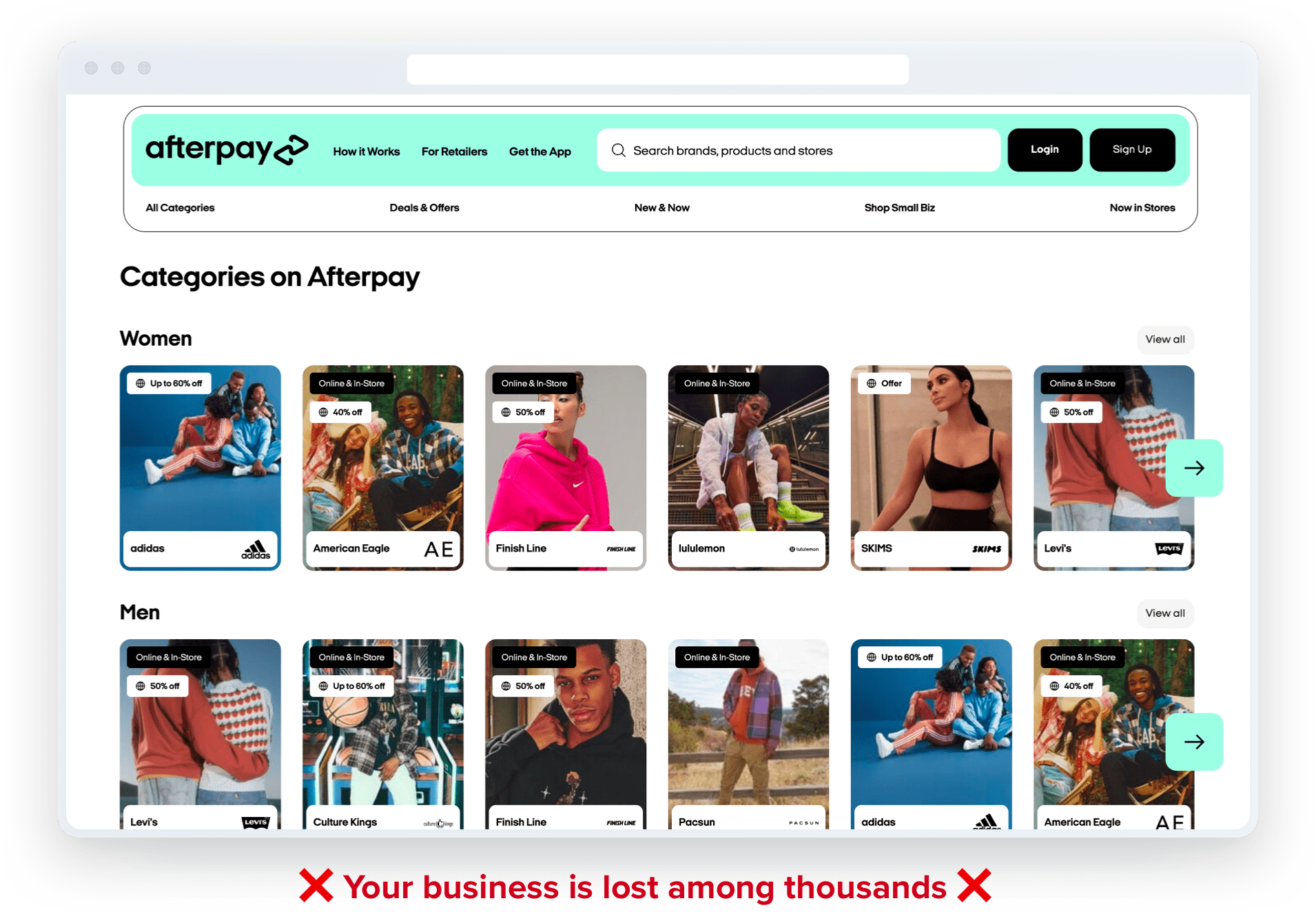

BNPL companies need volume – they need millions of customers using them every day to make money. This leads to them promoting their own platform and site as a shopping destination for your customers. They have shareholders to keep happy and lofty valuations to justify.

This means your customers, who you worked hard to acquire, are more likely to go to afterpay.com or klarna.com instead of your site for their next shop. On these sites, your business is just one of thousands, and your previously loyal customers are easily distracted by bigger brands, competitors, and deals.

Outsourcing customer financing can be the right approach for you depending on where you’re based, where your customers are based and the type of product you sell. This approach can be more suitable than doing it yourself if you have access to and are eligible for a deeply integrated solution – eg: if you are a Shopify Merchant based in the US, with customers also based in the US, and your average order value is not higher than their limit, Shop Pay Installments is a great product.

One critical consideration if you’re eligible to use BNPL companies like Afterpay, Klarna and others is how much you value your customer relationships. How expensive is it for you to get new customers? Because you’ll need them.

Once a customer has made a purchase using one of these providers, the emails they get are from the buy-now-pay-later company, and not your business. This slowly helps turn your customers into their customers and puts their brand front and center, instead of yours. If you’re a small business trying to build a loyal customer base, consider how much control (of your customers, pricing and brand) you’re willing to give up in exchange for getting paid upfront.

We have a detailed side-by-side comparison of BNPL vs. doing it yourself with easy software at the bottom of this page. Go there now.

Outsource customer financing to a traditional customer financing provider (clunky and outdated)

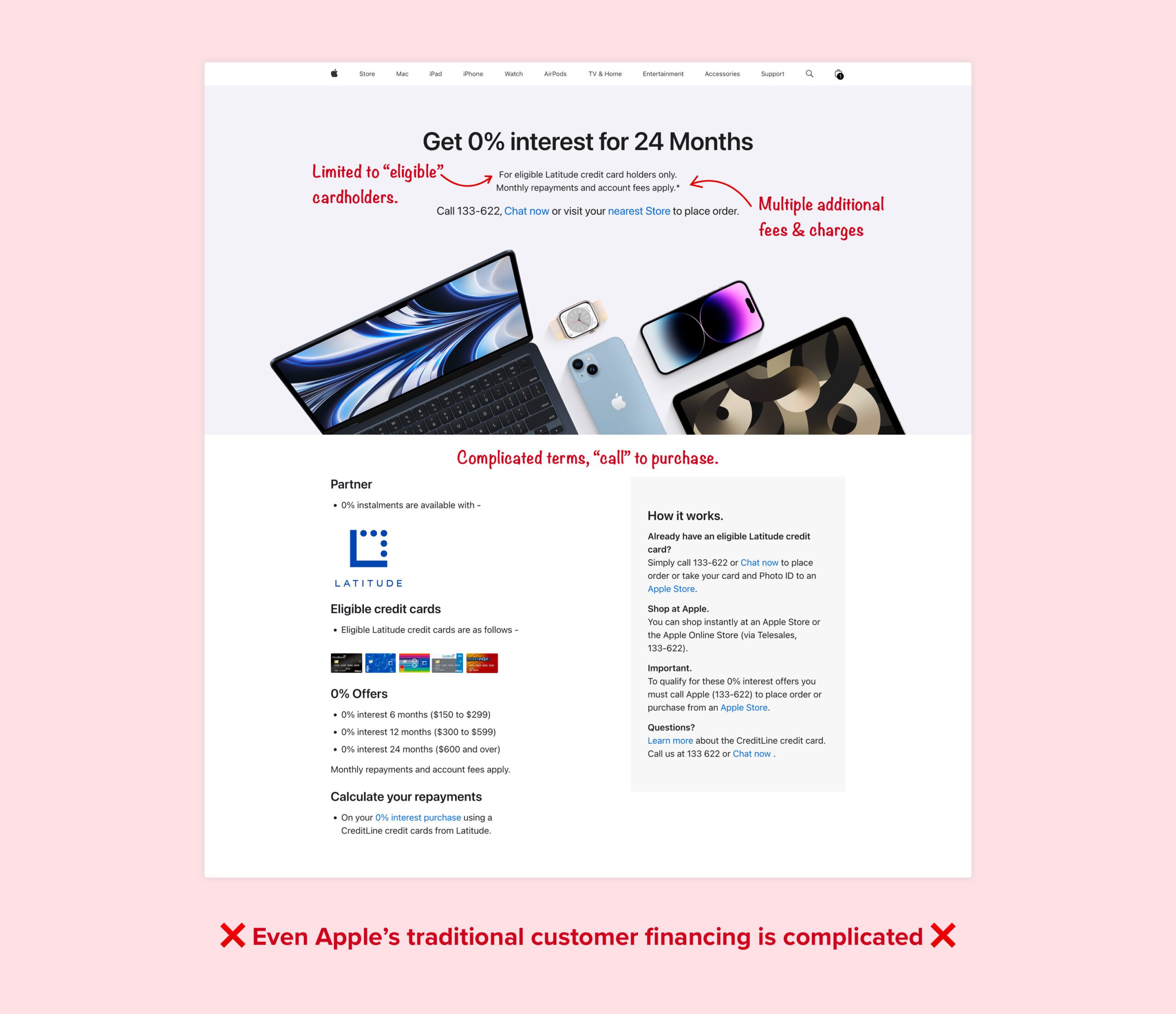

There are other, more traditional customer financing providers too but they typically have a poor customer experience, and clunky, long approval processes for customers. We won’t cover these in too much detail because of how limited they are. We don’t recommend these for most small and medium sized businesses (since most won’t even work with you without a large annual $$$ volume commitment).

These traditional consumer financing providers typically require you to contact them to schedule a call or demo, then talk to a salesperson, in some cases pay an “implementation fee” and in all cases, their pricing is “on request”.

This lack of transparency and clarity are big red flags for any small and medium sized businesses that like to be agile, offer great customer experiences and want transparent costs. These companies can makes sense as an option for large businesses but even then, they are extremely limited in terms of eligibility, and usage and deliver a very sub-par experience for customers. Even Apple, outside the U.S. has an extremely clunky and limited customer financing option (where available).

Offer your own customer financing (lower fees, maximum control)

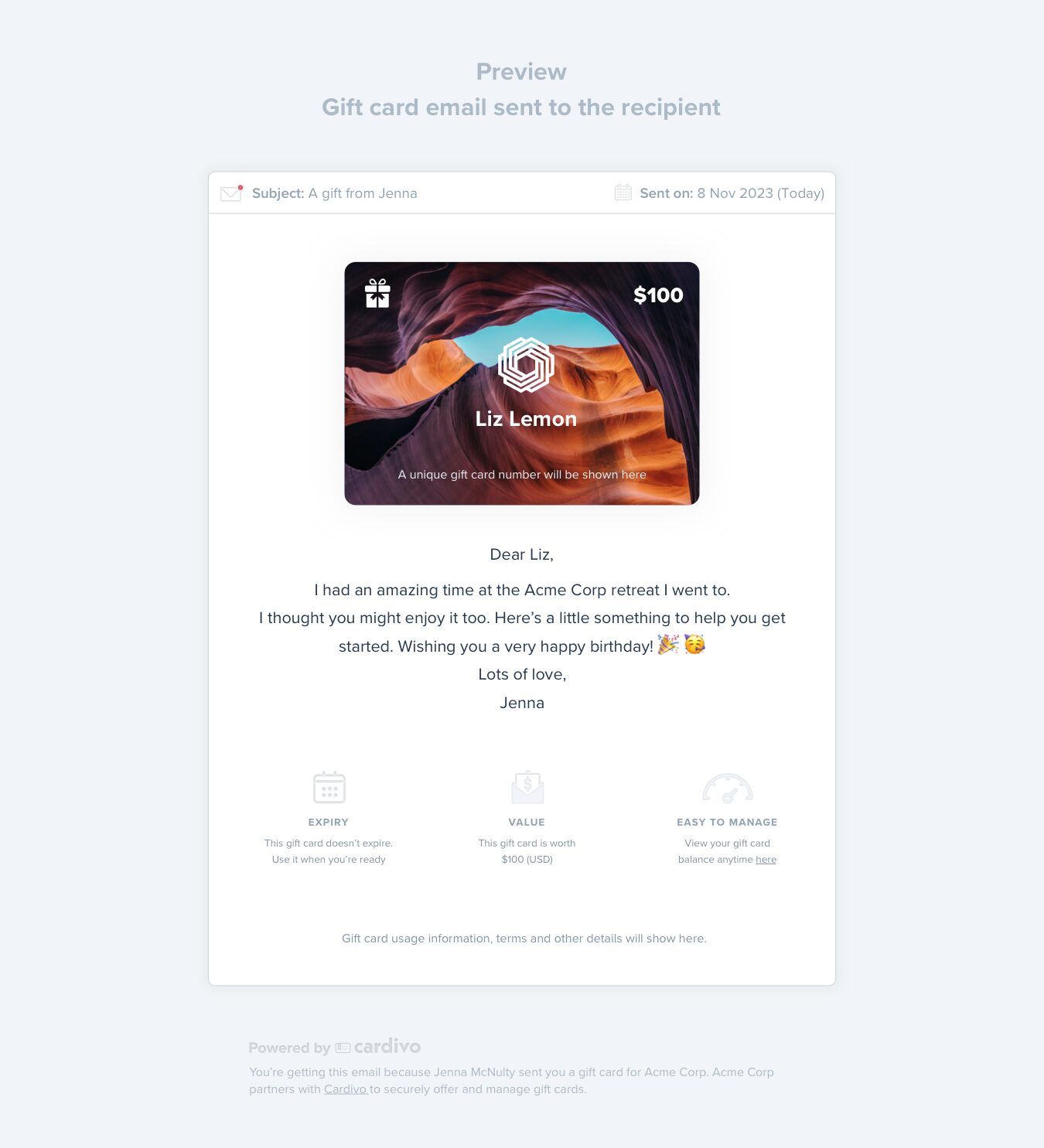

We’re biased, but we recommend most businesses should consider offering their own customer financing. In the past, this would have been a complicated and expensive exercise with much additional admin. However, with easy customer financing software like Paythen, this is very simple and mostly automated to manage, with minimal added admin.

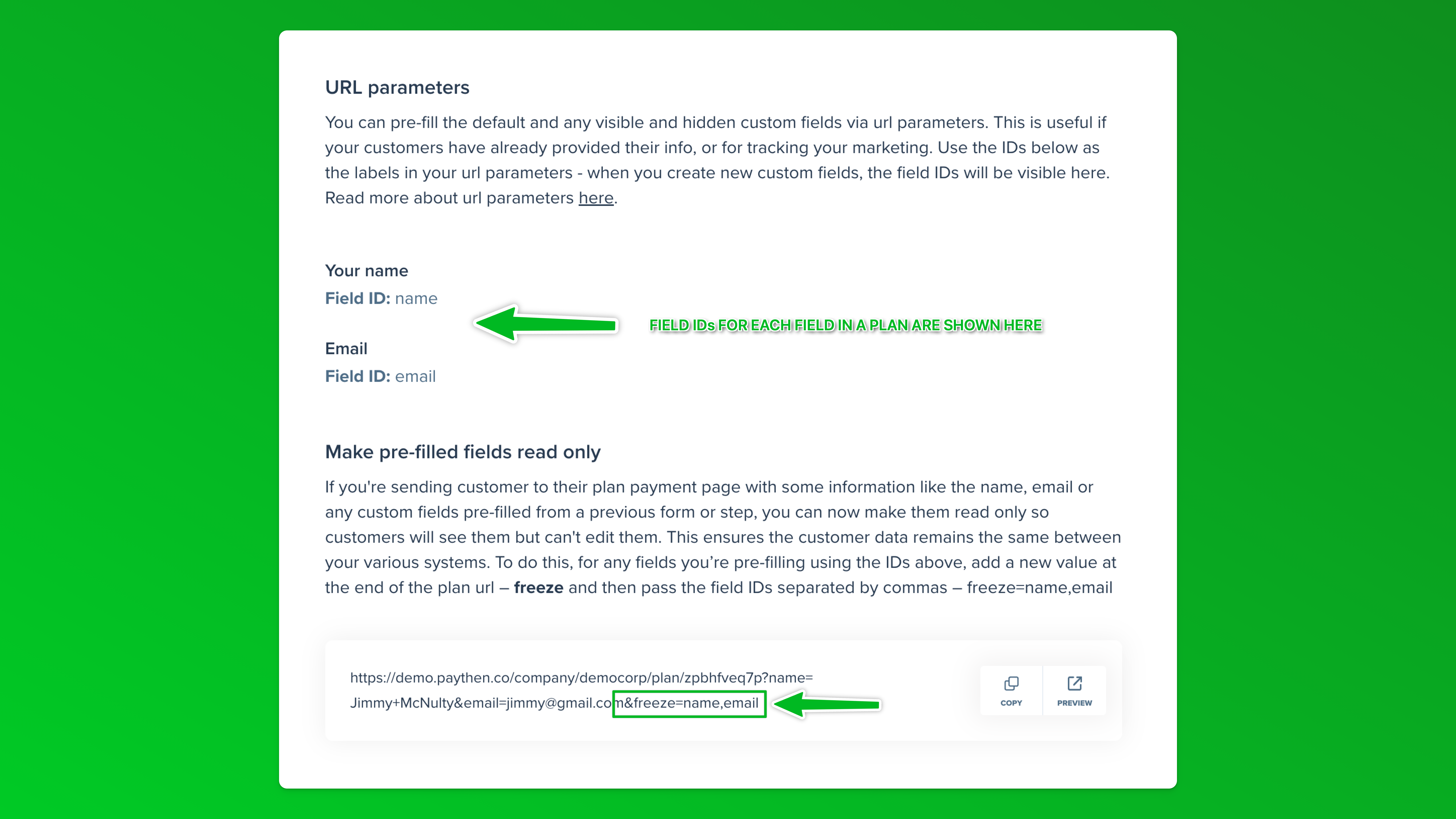

By offering your own customer financing, you retain full control of your brand, your customer relationships, and the flexibility to offer financing exactly how you’d like – with fees, billing intervals and any terms you set.

Paythen automates the process and gives you a full admin dashboard so you can easily track everything. With this approach, you can offer financing to all your customers anywhere in the world, and even in different currencies.

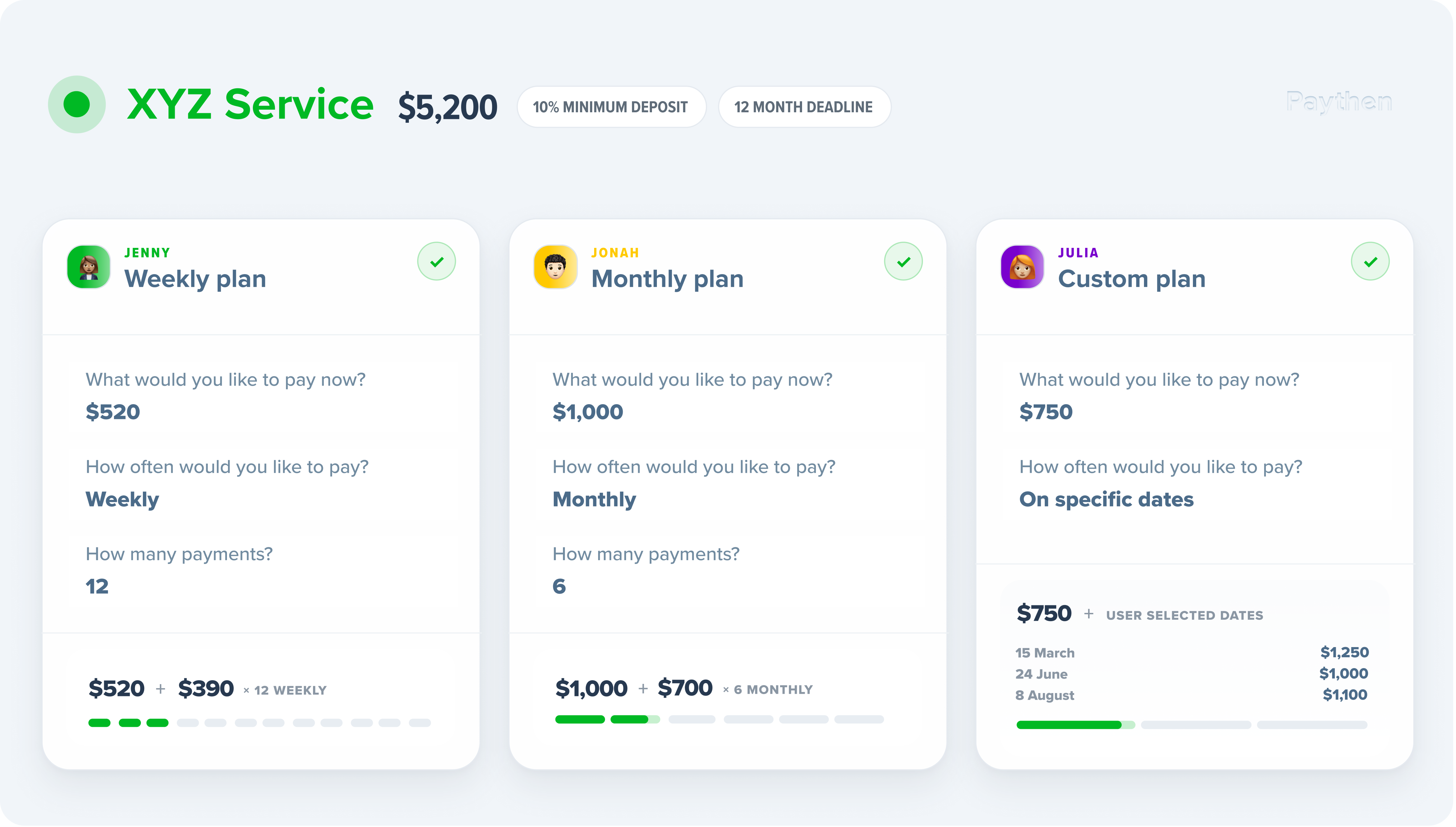

You can choose to add surcharges and additional fees, incentives to repay early, discount codes, billing intervals that work for your business – whether it’s 8 weeks, 6 fortnights, 12 months, and much more.

When you choose this approach, you remain in control of your customer relationships, and your brand. All emails and customer-facing pages contain your logo and colors and there is no platform trying to take your customers away.

Unlike the BNPL or traditional customer financing approach, most businesses across the world, with customers based anywhere, can use this. The only criteria is you have to be able to open an account with Stripe to process payments. Stripe is available to businesses in 47 countries and your customers can be in any country. Even businesses that are not in supported countries can use Stripe with Stripe Atlas.

Paythen doesn’t require code, or even any technical know-how. It is plug and play and takes only a few minutes to set up.

If you’re looking for a way to offer customer financing but want to retain control of your pricing, your customer relationships and your brand, Paythen may be the right tool for you. We have a fee-free 7 day trial, then just a low 2% per transaction with no other fees or charges. No credit card needed.

As with all billing systems, this is separate to the Stripe payment processing fees which are typically between 1.6% and 2.9% depending on your country. Paythen works with and requires Stripe to process payments. You can connect your existing Stripe account or create a new one easily when you sign up for Paythen.

Stripe is the world’s leading payment processor — they handle the underlying payment infrastructure to ensure your customers’ payment information is secure. Millions of businesses across the world use Stripe as their payment processor. Paythen works with, and requires, Stripe. When you start your free Paythen trial, you can connect your existing Stripe account or create a new one in seconds. Paythen is a Stripe verified partner.

Paythen is available anywhere Stripe is. If you can sign up for a Stripe account, you can use Paythen. Stripe is currently available to businesses based in over 40 countries (please see notes below for 'preview' countries), and almost anyone anywhere through Stripe Atlas. These are the countries supported by Stripe (and Paythen) at the moment:

You can accept payments in most currencies Stripe supports (over 130) – at the moment you can't accept zero decimal currencies with Paythen. There are some exceptions and limitations based on your account's currency. View the full list and more info here.

Are you in a country where Stripe is in preview?

Countries that show "Preview" above might have limited functionality as Stripe is just getting started there.You can read more about each supported country, including Stripe fees and sign up for a Stripe account here. Different preview countries might have different limitations.

For some countries, because of legal and Stripe restrictions, Paythen fees cannot be automatically deducted from each transaction like they usually are. In these cases, you can still use Paythen as normal – but your billing will be done monthly at the end of each month via a credit or debit card.

For some preview countries (like Indonesia and the Philippines), Paythen might only work if you have set up a Stripe account using Stripe Atlas but not if your account is based in your home country and currency. This is because of legal limitations in these countries that don't allow external platforms based in other countries to connect to locally-based accounts.

Is your Stripe account based in Japan?

Japan based accounts can use and accept payments with Paythen in all other currencies except JPY at the moment. Paythen does not support zero decimal currencies at the moment but we expect to add support in the future.

Is your Stripe account based in India?

Accounts based in India can currently only accept payments in INR using Paythen – we will be adding support to accept other currencies too, but at the moment, only INR payments can be accepted. If you're using Stripe Atlas with a USD account, then this does not apply.

Is your Stripe account based in Indonesia or the Philippines?

Unfortunately at the moment, due to legal and/or Stripe limitations, Stripe accounts based in Indonesia or the Philippines cannot connect to platforms like Paythen that are based in other countries, like Paythen is. We hope to support both countries in the future if and when this changes. You can use Paythen if you have a US based Stripe account created via Stripe Atlas though.

If Stripe is not available in your country, we recommend looking into Stripe Atlas. It's a great way to form a US company remotely and get all the benefits that come with it.

No. Paythen is not a buy now pay later credit service like AfterPay. We use AfterPay as an example below, but the points below apply to most buy now, pay later services like Klarna, Affirm and many others.

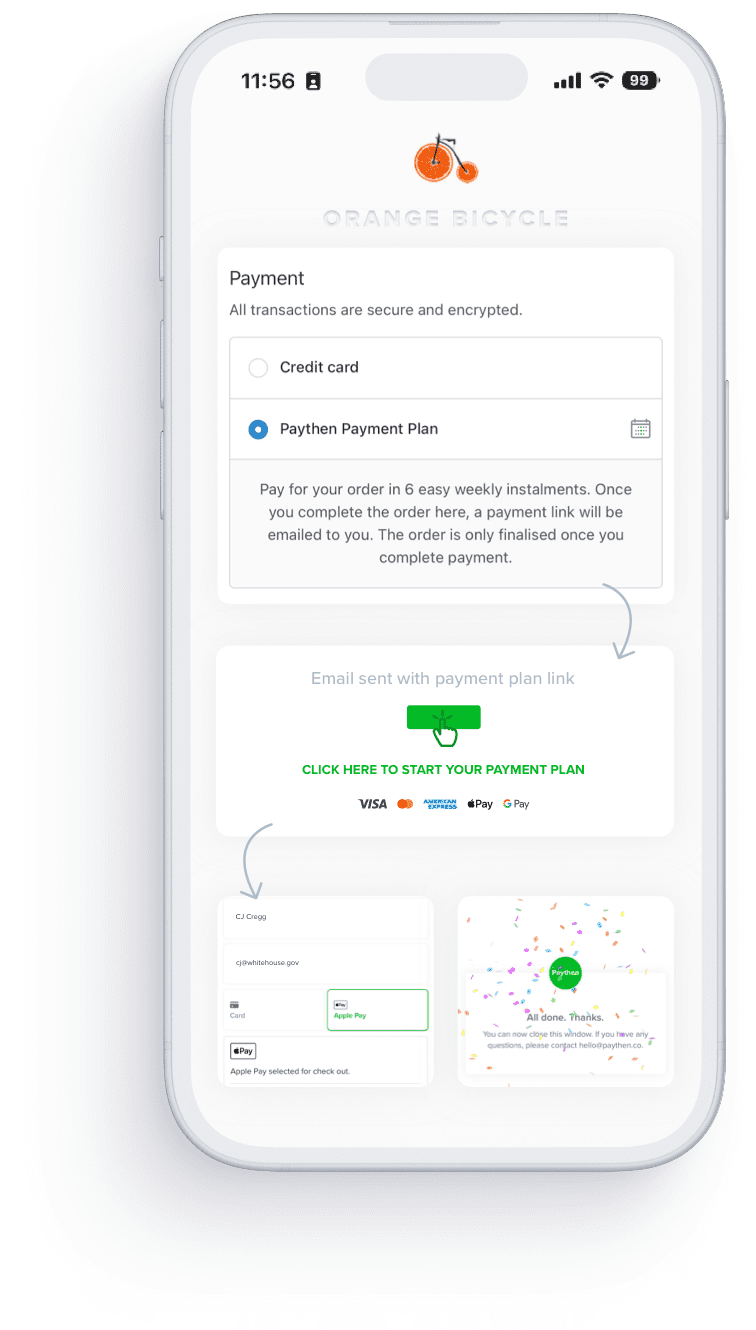

Once you create a plan in Paythen, your customers get to choose to pay the full amount immediately or via a payment plan that you've defined. Both options require your customers to use their credit or debit card to pay. This means 100% of your customers can choose a payment plan option instead of only those that get approved for credit.

- AfterPay is a credit service. With Paythen, your customers can get get a payment plan, but they can use their existing credit or debit card to do so.

- AfterPay is like a mini-loan, with Paythen, there is no credit provided – this is not only more responsible, but also more flexible and better. Your customers get to choose how they want to pay, and which payment method they want to use, while you pay lower fees and deliver a better customer experience.

- AfterPay has a fixed 8 week repayment period. This is rigid, and can still be very high for high value items. With Paythen, you can set the payment plan interval to whatever you want – weekly, monthly, fortnightly, or any other custom interval – and you also choose how long it goes for.

- AfterPay takes away your direct relationship with your customer – and build their brand, instead of yours. With Paythen, there is little to no Paythen branding involved – we just give you the mechanism to offer split payments, while giving you the reporting and flexibility you need.

- AfterPay takes away a big chunk of your profit margin with each transaction. With Paythen, you get to decide – you pay a low 2% per transaction with no monthly or other fees. You do pay the payment processing fee to Stripe, which is the payment processor.

- Paythen is a complete billing and payment system that gives you ease of use, reporting and insights and important features for your customers whereas AfterPay and others are just credit providers.

- Paythen is built on top of Stripe – the world's most popular (and in our opinion, the best) online payment processor. This means from day one, you can accept payments in hundreds of currencies.

We go into more depth on the comparison as well as the pros and cons of BNPL vs Paythen in this article.

Yes it does. The Paythen WooCommerce plugin is now available for all Paythen users. Read more about our WooCommerce functionality here. If you're interested in using the WooCommerce plugin, just create your free Paythen account, switch ON the WooCommerce integration, and install our WordPress plugin. Here's a step by step guide.

The current version of the Paythen WooCommerce plugin will let you offer a Payment Plan option on the checkout page. You will have defined some parameters of the payment plan beforehand. Here's an overview:

- You install our WooCommerce plugin and configure a few options

- On the checkout page, your customers will see a new payment plan option

- They will place the order and be taken to the Paythen plan page to complete payment. Your WooCommerce order status will be "On-hold" while they complete payment.

- Once they have successfully signed up to the payment plan, they'll be brought back to the WooCommerce order confirmation page and the order status will change to "Processing".

- Customers will get an email from Paythen with their payment plan details and dates, in addition to any emails you have configured in WooCommerce

- You can see their payment plan and information in the Paythen dashboard

- Your customers will be automatically charged for each future payment

Start your 7 day free Paythen trial to see if it's right for you.

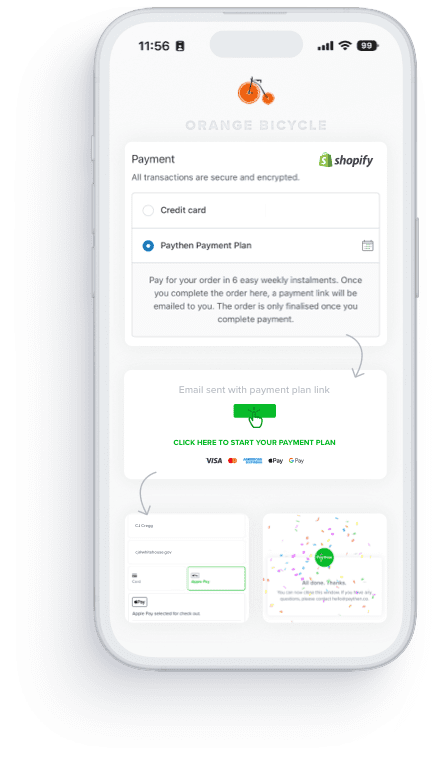

Yes, but with an email based workflow. There is no Paythen app for Shopify because of limitations imposed by Shopify. Your customers will get an email with a link to start their payment plan after completing the checkout on your Shopify store. Read more here and check out our Shopify demo store.

Here’s a side-by-side comparison of outsourcing your customer financing using BNPL providers vs. offering it on your own with Paythen:

| Outsourcing your customer financing with BNPL | Maintaining control of your customer financing with Paythen | |

|---|---|---|

| Fees | You pay a lot – usually between 6% and 12% depending on the provider and country. In many industries, this can be a huge part of your profit margin. For longer terms beyond 8 weeks, your customers can pay a high interest rate too. | You pay only 2% + Stripe fees |

| Who pays for the fees | Most providers make you sign a contract stating you won’t charge extra for their services – forcing you to absorb their fees. This is inherently wrong. You work hard to build your business and brand. A payment provider shouldn’t try to dictate what you can and can’t charge your customers. | With Paythen, if it makes sense for your business, you can easily add a surcharge to cover fees or other expenses. You can charge this fee over the payment plan, or upfront. You’re in total control. |

| Country availability | Most providers are available to businesses in certain countries only. Even the biggest ones are only available if you’re based in a handful of countries. Your customers must also be based in the same country. | Available to businesses in 40+ countries with customers anywhere in the world. |

| Eligibility | You need to “apply” and get approved. Only businesses operating in certain industries are eligible. Your customers also need to apply and get approved. In some cases, they must also complete credit checks. | Get started in under one minute – no approvals needed. All businesses across all industries can use Paythen. All your customers can use Paythen with their existing credit or debit cards. |

| Cart value | Most providers restrict the total credit available to customers to between $1,000 and $1,500. If you sell a higher value product or service or if customers have other purchases on a payment plan, they can’t buy what you’re selling. | With Paythen, there are no limits to the total order value so you can sell high value items without limits. In fact, most Paythen customers sell products and services over $1,000. |

| Flexibility | None. Each provider typically has a fixed repayment period – typically between 4 and 8 payments spread over 1 to 4 months. If this doesn’t suit your business, tough luck. For many businesses selling a high value service or product, the amounts per payment can still be quite high, reducing sales. | With Paythen, you have a lot of flexibility – set billing intervals weekly, fortnightly, monthly, or anything you want. Set repayments to be over a few weeks, months or even years if you need. Collect a larger amount upfront, add surcharges, hidden fields, and more. |

| Payment currency | You can only charge in your home currency. | Offer customers payment plans in 130+ currencies. |

| Your brand | Your brand takes a backseat to their brand. All communications and user interactions are from their brand. They build their brand at your expense. | Paythen lets your brand shine while handling the back-end admin for you. Your customers see your branding – your company name, your logo and your colors. |

| Your customers | Once your customers sign up to use one of these services, they essentially become their customer. You lose any direct relationship with the customer, and over time, the providers focus heavily on driving all customers to their home page, not yours. You basically pay these providers in dollars as well as customers. | Your customers are always yours. Paythen is software designed to help you provide a seamless payment plan experience. We don’t want your customer relationships.With Paythen, your customer communications and data are always fully controlled and owned by you. |

| When you get paid | You get paid the full amount upfront, less a big chunk of fees. | You get paid as your customers pay, with automated reminders and follow-ups that handle any failed payments. |

| Types of payments | One option only – their fixed payment plan. If you want to sell other types of services or products like subscriptions, you have to mix and match payment providers. | With Paythen, in addition to payment plans, you can offer subscriptions, one time payments, and our unique Pay your way plan that lets your customers choose to pay in full or via a payment plan, for the same product. |

| Where you can accept payments | Limited. You can only use these providers in your ecommerce or physical store. | No limits. Each plan in Paythen gets its own unique payment link that works everywhere – on your website, socials, WhatsApp, text messages, and anywhere your customers are so you can use Paythen in any context. |

| Reporting | Limited reporting on just a portion of your customers. | Unified reporting in a beautiful dashboard that lets you understand what you’re owed vs. paid, and lots more. |

While we are biased, we believe setting and controlling your own customer financing, with your own branding, and critically, your own customer relationships, is a better option for many businesses. The fact that you pay significantly lower fees makes it even better. For certain types of businesses where you must get paid the full amount upfront, despite higher fees and less control, a buy now pay later provider might be more suitable. In fact, some customers even use both Paythen and a buy now pay later provider for different contexts.

The best way to see if Paythen is the right fit for you is to try it out. There’s a 7 day fee-free trial and it takes only a few minutes to get started. If you have any questions, or need a hand getting started, just reach out via the chat icon or email hello@paythen.co – we’d love to help.